")

Introduction to Valuation

Venture capital firms currently use three primary valuation methods – the Berkus method, Relative Valuation, and Scorecard. For revenue generating startups more complex valuation models like Book Value and DCF come into play. Let’s try and understand what goes into each of these.

Berkus Method

Berkus method is one of the most popular valuation methodologies specifically for pre-revenue companies. If your business is still in the ideation or prototyping phase and you feel the idea is innovative enough to garner interest among investors, it may be worthwhile to try and estimate the value of your company based on the revenue generation potential of the idea and product.

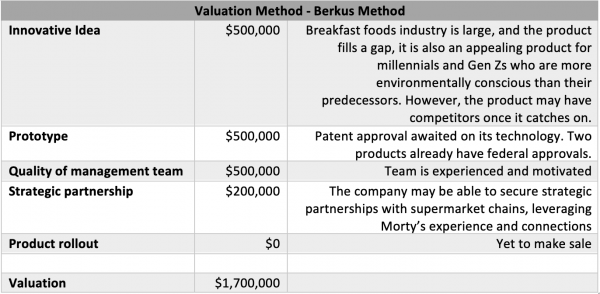

We will use an example to illustrate how this works. Suppose Company X wants to revolutionize the Canadian nutrition industry. They have an idea for a protein and nutrients heavy shake and energy bar that is manufactured using insect proteins. The idea is fairly innovative and will be a godsend for people who are unable to use traditional protein products that use soybeans or milk whey as base ingredients. The founder, Diana Moretti, has a highly qualified team – she is a practicing a nutrition professional in Toronto, her chief product office Francisca Lin served as a food technologist at a leading nutrition brand for 15 years prior to co-founding Company X, and her Sales Lead, Morty Blank has a huge network of connections in food & beverage space courtesy his wide-spanning cross-geographical experience in sales across various CPG brands in Canada.

Diana, Francisca and Morty co-founded Company X with contributions from their own personal savings which have mostly been used towards prototyping and testing three specific products they can launch into the market. The company already has federal approvals for two of its products. However, they will require capital to start manufacturing them at scale, as well as for the launch and marketing of its brand.

Let’s try to value Company X as it stands. The maximum value for each of the parameters under Berkus Method is 500,000, which means that the maximum possible value for the Startup is $2.5 million. Based on the Berkus method, Company X can be valued at $1.7 million. It should be remembered that you will need to do a deep-dive of the market to place the value of each of these parameters. For instance, the valuation of the management team derives from the market value of these individuals based on their past credentials and the money they would otherwise be able to demand in the market based on their executive skills. The value of the innovative idea will depend on a number of factors – is it easy to duplicate, what is the potential market size of the product, how much of the market is potentially being targeted and so on.

Based on the Berkus method, Company X can be valued at $1.7 million. It should be remembered that you will need to do a deep-dive of the market to place the value of each of these parameters. For instance, the valuation of the management team derives from the market value of these individuals based on their past credentials and the money they would otherwise be able to demand in the market based on their executive skills. The value of the innovative idea will depend on a number of factors – is it easy to duplicate, what is the potential market size of the product, how much of the market is potentially being targeted and so on.

Risk Factor Summation

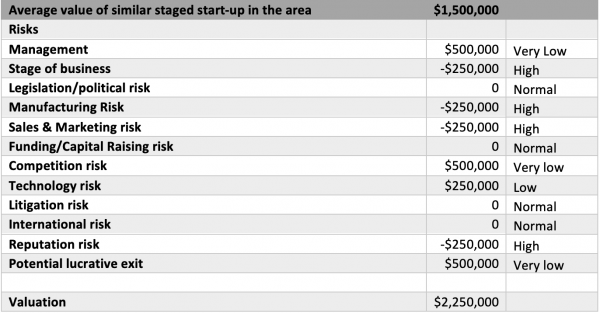

Relative valuation, as the terms suggest, is derived from assessing risk factors for a startup. These may differ depending on the type of business.

The valuation is simple but quite subjective – start with an initial valuation of 250,000 (or a multiple thereof) and then increase or decrease that monetary value in multiples of $250,000 based on risks factors that may affect your startup. If you have very low risk, you can add up to $500,000, but if the risk is too high you’ll need to subtract the same amount. The total value will then be added or subtracted from the average value of a similar startup (in the same stage) in that geographical area (this information is available on platforms like the Bloomberg Terminal, Crunchbase or the PitchBook).

Let’s try and value Company X based on this method.

This method yields a valuation of $2.25 million. But careful, this number would be highly dependent on the average valuation of other similar startups as well as the perception of risk on each of these factors.

The Scorecard

The Scorecard method is a back-of-the-envelope valuation method for very early-stage startups. It is similar to the Berkus method is many ways. In this method, depending on the industry, geography, and type of business you allocate value to each of the parameters listed below and then rank your own business on each of these parameters. Let’s try to value Company X on the grid below:

Based on the Scorecard, the valuation is $1.6 million.

Now that we have discussed valuation methods for pre-revenue startups, let us look at some of the ways we can value companies that have started generating revenue. Traditionally, accountants use two methods to value businesses: Book Value and Discounted Cash Flow. We’ll delve into each of these here.

Book Value

This method is outdated and is only sparingly used to value startups. Essentially, book-value method gives you an asset-based valuation, which is equal to the total assets of the company (manufacturing plants, real estate, receivables etc) minus its total liabilities (payables, outstanding debt etc). However, book value fails to capture the potential revenue of a company once it has scaled to achieve economies of scale. Entrepreneurs should avoid using the book value method when pursuing equity investments.

Discounted Cash Flow

We use the discounted cash flow (DCF) method for relatively more mature businesses with steady cash flows. For newer businesses, especially those driven by technology and with a high potential Return on Interest (ROI), VCs may use the DCF in conjunction with other methods to gauge the true value.

To calculate DCF valuation you take the forecasted future cash flows of the business and apply a discount rate, or the expected rate of return on investment (ROI). This is a little more complicated endeavour and requires a bit of accounting knowledge. But fear not, there are plenty of resources to help you navigate the process – refer to the CFI resources on DCF calculation here.

There are three things you need to understand before calculating firm valuation with this method –

- Growth rate: You’ll need to calculate the expected rate at which the company will grow over the foreseeable future (forecast period). This will determine the value of future cash flows . Calculating growth rate can be hard for startups given that they are relatively new and fast evolving and therefore lack reliable historical data that can be used as base for the calculations – in such cases it can be useful to derive this value from past startups with similar growth trajectories.

- Discount Rate: Discount rate is basically pricing in inflation to ensure that we have a true value of future cash flows. Basically, as inflation rises and the cost of borrowing money goes up, the amount of goods that can be bought with that money decreases – what this means is that inflation reduces the true value of this money. With an estimate of the discount rate, we try to include potential rises in the cost of borrowing as part of our calculations.

- Terminal Value: Once we have obtained the free cash flow values and the discount rate, we can use these values to calculate the Terminal Value of the business. Terminal value, in simple terms, is the value of the business beyond the forecast period. Say the forecast period is 10 years and based on the growth rate you have already determined the free cashflows over this time. We would assume that beyond the 10 years, your business will grow at a fixed growth rate forever – even after the forecast period.

Now that you have all these values, you simply need to plug them in to calculate the DCF valuation. You can use a handy spreadsheet like the one available here.

Further, you can also perform Sensitivity analysis to calculate valuations if the business fares better or worse than expected.